It is an incredibly tough time to launch a fast-moving consumer goods (FMCG) brand. Globally, the odds are already stacked against innovators: a landmark European study by Nielsen (NIQ) analyzed over 12,000 product launches and revealed a sobering reality—76% of all new FMCG products fail to survive their very first year on the shelf.

In Egypt’s current economic climate, that margin for error shrinks to zero.

Between currency fluctuations, shifting household budgets, and a massive consumer wave pivoting toward local alternatives, launching a product based on “gut feeling” is a fast track to a costly write-off. To succeed in Cairo, Alexandria, and beyond, brands must move past generic marketing theories. You need a rigorous, highly localized validation process.

Below is the first critical step of our battle-tested, 6-step FMCG validation framework, designed specifically to help your brand launch with absolute confidence.

Step 1: Decoding the Egyptian Grocery Basket (Consumer Empathy & Pantry Audits)

The classic “Empathize” phase of product development cannot happen behind a laptop in a Smart Village office. It has to happen inside Egyptian kitchens.

Economic pressures have turned the modern Egyptian household manager into a master strategist. Rising inflation means that she is actively auditing her grocery bill every single week, separating household items into strict “non-negotiables” (baby formula, basic cooking oil, tea) and “disposable luxuries” (imported snacks, premium detergents, niche condiments). To build a product she will actually buy, you have to understand this mental split.

The Actionable Validation Playbook

To truly decode her needs, swap out standard online surveys for high-empathy field research:

- In-Home Pantry Audits: Secure permission to visit kitchens across different demographic segments—from middle-income apartments in Imbaba to upscale villas in New Cairo. Open the cabinets. What you see on the shelf is the truth; what people claim to buy on a survey is often idealized. Look for where imported brands have been swapped out for local alternatives (e.g., local Egyptian dish soaps, local coffee blends, or domestic biscuit brands).

- Contextual Focus Groups: Don’t just ask, “Do you like chocolate?” Ask, “Walk me through the exact moment you decided to buy this local snack instead of Cadbury. How did you feel about the trade-off?” Identify the exact emotional compromises they are making.

⚠️ A Historic Lesson on Skipping Step 1: The “New Coke” Disaster (1985)

When Coca-Cola decided to launch “New Coke” in 1985, they believed they had validated the move perfectly. They ran over 190,000 blind taste tests, and consumers consistently preferred the sweeter new formula over the classic taste.

Yet, the launch was one of the most famous failures in retail history. Why? Because Coke skipped deep emotional empathy. They treated their product as a mere liquid in a can, failing to realize that classic Coke was deeply woven into the cultural identity and childhood memories of their consumers. The emotional backlash was instant, forcing them to pull the new formula within 79 days.

The Egyptian Parallel: If a local Egyptian dairy or snack brand reformulates a beloved classic or launches a new product line using cheaper local fats to save on raw material costs—even if laboratory taste-testers say it’s “close enough”—they risk catastrophic consumer backlash. In Egypt, food is deeply tied to family, comfort, and tradition. Violate that emotional connection without empathy, and consumers will permanently walk away.

Step 2: Mapping Gaps in the Local Egyptian Retail Shelf (Defining the Opportunity)

Once you have empathized with the Egyptian household planner, you must translate those raw consumer insights into a defined, mathematically viable product-market fit. In product development, a major trap is defining the opportunity too broadly (e.g., “Egyptian consumers want cheaper snacks”). You must identify the exact whitespace on the physical shelf that competitors are ignoring.

In Egypt’s current retail climate, massive gaps have opened up due to two macro-trends:

- Import Substitution: High tariffs and currency devaluations have priced premium imported brands out of the reach of the average consumer.

- The Rise of Local Pride: Consumers are actively seeking domestic, high-quality alternatives that respect their heritage and their wallets.

The opportunity isn’t just about making a cheaper copy of an imported product; it is about defining a new “accessible premium” tier.

The Actionable Validation Playbook

To map and define these retail gaps scientifically:

- Price-Pack Architecture (PPA) Benchmarking: Audit the target category across major chains like Seoudi and local neighborhood kiosks. Map out the price per gram or price per milliliter of every competitor. You will often find a gaping hole—for example, plenty of ultra-cheap, low-quality local options, and very expensive premium imports, but absolutely nothing in the high-quality, mid-priced tier.

- The “Unmet Need” Matrix: Align your product specs to solve a specific, defined structural pain point. If your Step 1 research showed mothers are frustrated by large packaging that spoils before their kids can finish it, your defined opportunity is not a new flavor, but a single-serve, re-sealable format priced under a specific psychological price threshold (e.g., 10 or 15 EGP).

⚠️ A Historic Lesson on Skipping Step 2: The “Gerber Singles” Flop (1974)

In 1974, baby food giant Gerber identified what they believed was a brilliant market opportunity. Their internal research suggested that college students, single adults, and elderly people living alone wanted quick, nutritious, single-serving meals.

To fill this gap, they launched “Gerber Singles“—jars of puréed adult foods in flavors like Beef Burgundy and Blueberry Delight, packaged in the iconic glass baby food jars.

As reported by CBS News and analyzed in brand equity studies (such as research published in the Journal of Brand Management), the product was an epic disaster and was swiftly pulled from shelves.

Gerber defined the opportunity purely as a utility gap (convenient single-serve meals) while completely ignoring consumer psychology. Adults, particularly single ones, found eating puréed food out of a baby jar to be socially embarrassing and unappetizing. The brand equity of Gerber was so deeply anchored in “infant nutrition” that it could not credibly stretch into adult cuisine.

The Egyptian Parallel: If an Egyptian company known exclusively for household cleaning detergents tries to bridge a gap in the personal care or cosmetics space under the exact same brand name, they will run face-first into the “Gerber Singles” effect. Egyptian consumers are highly brand-sensitive. You must define your product opportunities where your brand has the emotional and logical right to win.

Step 3: Co-Creating Flavors and Formulations with Local Consumers (Ideation)

Once you have defined your target pricing and identified the exact shelf space you want to capture, it is time to develop the actual product. In traditional FMCG development, this step usually happens in a closed corporate boardroom. A group of marketers and food scientists look at global trends and decide what flavor or scent to launch next.

In a complex, culturally rich market like Egypt, this insular approach is highly risky. To build immediate brand equity, you must invite your consumer into the kitchen. Co-creation transforms the consumer from a passive target buyer into an active stakeholder in the product’s success.

The Actionable Validation Playbook

To successfully execute collaborative ideation in Egypt:

- Interactive Co-Creation Workshops: Bring together groups of target consumers (e.g., college students for a snack launch, or mothers for a dairy launch) and put actual ingredients in front of them. Let them mix, match, and propose flavor profiles. In Egypt, there is a powerful tension between nostalgic local profiles (such as meshabek, roumy cheese, or hibiscus) and westernized trends. Let the consumers map out where your product should sit on this spectrum.

- Localized Crowdsourced Ideation: Use social media polls and interactive campaigns to narrow down potential concepts. This serves a double purpose: it validates real consumer interest in specific flavors before you spend on R&D, and it builds early viral buzz.

🏆 A Success Case: Lay’s “Do Us a Flavor” (Chipsy Egypt)

When PepsiCo needed to “age down” its audience and boost engagement with younger demographics, it launched the global “Do Us a Flavor“ campaign (historically adapted in Egypt under PepsiCo’s local Chipsy brand).

Instead of guessing what flavors the next generation wanted, PepsiCo handed the keys to the consumer, allowing them to submit ideas via social media. The public then voted on the final flavors.

According to a Wharton School of Business case study and Penn State brand analysis:

- The first campaign yielded over 3.8 million flavor submissions (shattering PepsiCo’s original estimate of 1 million).

- During the campaign, the brand’s year-over-year sales surged by 12%, and the winning flavor (“Cheesy Garlic Bread”) drove an immediate 8% sales boost in the three months post-launch.

- The campaign succeeded because PepsiCo gave consumers genuine ownership over the product portfolio, creating a highly localized, responsive development model.

⚠️ A Failure Case: The Kraft “iSnack 2.0” Backlash (2009)

While co-creation is powerful, you cannot fake it. In 2009, Kraft Australia wanted to launch a new, creamier blend of its iconic breakfast spread, Vegemite. They ran a massive “Name Me” campaign, receiving over 48,000 public submissions.

However, instead of letting the public vote on the final winner, Kraft’s internal panel of marketing executives bypassed the crowd’s favorite suggestions and hand-selected a highly corporate, tech-sounding name: iSnack 2.0.

As documented by Harvard Business School’s Digital Innovation and Transformation case repository and the Journal of Brand Management:

- The public reaction was immediate, fierce, and highly negative. Consumers felt the tech-themed name (“iSnack”) was a cold, corporate gimmick that insulted a beloved national food icon.

- The media backlash was so severe that international outlets ridiculed the decision, prompting threats of a consumer boycott.

- The Rollback: Kraft was forced to issue a public apology and abandon the name just four days after announcing it, spending millions to rapidly rebrand the product to “Vegemite Cheesybite.”

The Egyptian Parallel: If you ask Egyptian consumers to help you co-create a new local beverage or food brand, you must honor their input. If you run a major public voting campaign on social media but then choose a name or flavor that feels like a disconnected corporate decision made in a boardroom, you will alienate the very community you sought to build. True co-creation requires transparency and trust.

Step 4: Rapid Packaging and Product Prototyping (Bringing the FMCG Concept to Life)

Once you have co-created your recipes, formulas, and visual concepts, you must bring them into the physical world. In the FMCG sector, a “prototype” is not a digital wireframe or a 3D render. It is a tangible product that a consumer can touch, open, smell, and taste.

This phase is where many Egyptian brands overspend. They rush into massive industrial production runs, renting factory lines for days just to produce “samples.” In today’s high-inflation climate—where packaging materials like PET plastic, aluminum, and paperboard are subject to volatile pricing—early industrial scaling without physical validation is an immense financial gamble.

Instead, you need to develop low-fidelity, cost-effective prototypes that mimic the final customer experience.

The Actionable Validation Playbook

To run lean prototyping in the Egyptian FMCG space:

- Mock-Up Kitchens & Local 3D Printing: Rather than hiring a commercial factory, use local Cairo-based rapid prototyping labs or culinary co-packing spaces to produce small-batch samples (50 to 100 units). Use 3D printing to create physical mock-ups of custom caps, bottles, or jars so you can test their ergonomics and “hand-feel” first.

- The “Cluttered Shelf” Test: Print high-quality mock-ups of your label designs and place them on a physical shelf inside a controlled testing room. Surround your prototype with actual competitors from Egyptian hypermarkets (like Carrefour, Spinneys, or LuLu). Invite consumers in and track where their eyes land first. If they fail to spot your product within three seconds, your packaging is functionally invisible.

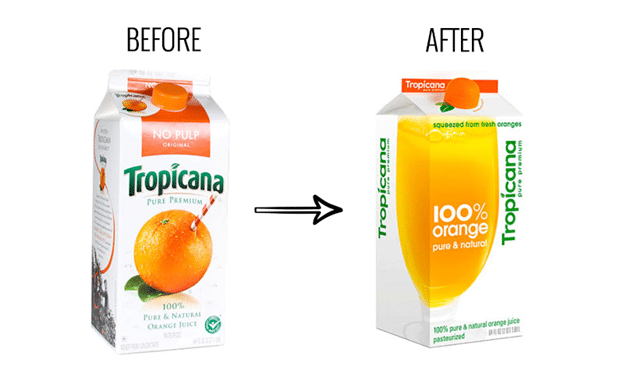

⚠️ A Failure Case: The Tropicana Packaging Disaster (2009)

In January 2009, PepsiCo-owned Tropicana decided to completely redesign the packaging of its best-selling orange juice for the North American market, investing over $35 million in a sleek, minimalist design.

Their new product development strategy was to replace the iconic orange with a straw sticking out of it with a clean, modern glass of juice, and changed the classic serif font to a clean sans-serif typeface.

According to an in-depth brand equity analysis published by The Branding Journal and case studies from the Harvard Business Review:

- The Retail Backlash: The new design was an immediate failure. Consumers found the new packaging cold, clinical, and confusing. Because the iconic orange was gone and the logo was turned sideways, shoppers literally could not find their favorite juice on cluttered supermarket shelves. Many mistook it for a cheap, generic supermarket store brand.

- The Financial Toll: Tropicana’s sales plummeted by 20% in just two months, representing a loss of roughly $30 million in revenue.

- The Retreat: On February 23, 2009—a mere 46 days after the launch—Tropicana announced they would scrap the new packaging and return to the original classic design, writing off millions in design and manufacturing costs.

The Egyptian Parallel: In Egypt’s highly competitive, fast-paced retail environments, visual shortcuts are everything. If your local brand launches a packaging redesign or a new line without physical shelf testing, you risk alienating consumers who rely on visual familiarity to make split-second decisions. If you strip away the familiar cues that Egyptians associate with quality (like rich colors, clear ingredient photography, or trusted local markers) in favor of overly sterile “global” aesthetics, your product will sit on the shelves gathering dust.

Step 5: Rigorous In-Market Testing Before the Nationwide Rollout (Test & Launch)

Once you have verified your physical packaging and product taste profiles in a controlled lab, you are ready to face the real test: the live retail shelf.

In the FMCG world, there is a massive behavioral gap between what a consumer says they will buy during a free focus group and what they actually spend money on when standing in a grocery aisle.

If you skip a controlled market test and immediately distribute your product to thousands of traditional bakkals (neighborhood mom-and-pop grocers) and modern supermarket chains across Egypt without clear new product development research, you risk a disastrous shelf failure. If the product does not rotate quickly, retailers will delist your brand, and reclaiming that lost shelf space is nearly impossible.

The Actionable Validation Playbook

To execute a low-risk, highly scientific market test in Egypt:

- In-Home Usage Tests (IHUTs): Distribute 100 to 200 fully packaged, finished products to a cohort of target households. Allow them to use the product naturally in their daily lives for a week. Follow up with a structured survey to calculate your Repeat Purchase Intent (RPI). If less than 70% of your test cohort expresses a strong desire to buy the product again with their own money, go back and refine the formula.

- The Single-Chain Pilot: Partner with a single, major modern retail partner (such as Seoudi, Hyperone, or a specific regional chain in Alexandria) for a 30-day exclusive pilot. Monitor the daily sales velocity and measure how well consumers respond to point-of-sale displays. This gives you real transaction data to prove demand before negotiating expensive listing fees (slotting fees) with national hypermarket groups.

⚠️ A Failure Case: Campbell’s “Soup Redefined” Flop in Russia (2011)

In 2007, Campbell Soup Company entered the massive Russian soup market. Because Russians consume an estimated 32 billion bowls of soup annually, the market seemed like a guaranteed goldmine.

Campbell’s spent four years conducting extensive consumer research, even sitting in over 100 Russian kitchens to watch homemakers prepare broth from scratch. Based on this, they developed a line of premium, wet, packaged broths under the “Domashnaya Klassika” (Home Meal) brand.

According to detailed market case studies from the Harvard Business Review and reports in Reuters:

- The Launch Mismatch: Despite years of qualitative research, Campbell’s rushed the product to a broad launch without validating actual purchasing behavior in a localized market pilot.

- The Cultural Blindspot: They failed to realize that while Russian homemakers valued convenience, cooking soup from scratch was a deeply prideful, non-negotiable family ritual. Purchasing pre-packaged, wet broth felt lazy and culturally inappropriate to the core target buyer.

- The Withdrawal: In 2011, after four years of poor sales velocity and high retail distribution costs, Campbell’s pulled the brand and completely shut down its operations in Russia.

The Egyptian Parallel: This is a powerful warning for brands launching in Egypt. You might research Egyptian culinary trends and create a product that sounds excellent in theory (such as a pre-packaged, ready-made traditional soup or sauce). However, unless you test actual purchase behavior in a live, localized pilot, you won’t know if the consumer’s deep-seated cultural pride in home cooking will override the convenience your product offers.

Step 6: Real-Time Shelf Monitoring and Formula Optimization (Post-Launch Audit)

Many brand managers celebrate the day their product ships out of the factory doors. They look at the initial sales reports—known in the industry as Primary Billing (the inventory sold to distributors and wholesalers)—and assume the launch is a massive triumph.

This is a dangerous illusion.

In FMCG, a launch is not successful when the distributor buys the product; it is successful when the end consumer buys it, takes it home, uses it, and returns to the store to buy it again. If you only track your warehouse shipments, you are flying blind. You will not realize the product is failing until months later when distributors suddenly stop ordering because their warehouses are completely choked with unsold inventory.

To survive post-launch, you must transition from tracking shipments to monitoring real-time, on-shelf consumer behavior.

The Actionable Validation Playbook

To run a rigorous post-launch audit in Egypt:

- Audit “Secondary Offtake” vs. “Primary Billing”: Work closely with your sales team to monitor the ratio between what you ship to distributors and what retailers actually sell to consumers. If your pipeline fill ratio stays high (e.g., 4:1) past the first four weeks, it means your product is sitting dead on retail shelves.

- Field-Force Store Audits: Deploy field agents or use retail execution apps to audit local bakkals and supermarkets. Check your Outlet Strike Rate (the percentage of active stores reordering your product) and monitor your actual shelf placement. If shopkeepers are tucking your brand behind established competitors, you need to immediately adjust your trade promotion schemes to incentivize eye-level placement.

- Localized Social Listening: Monitor highly active Egyptian consumer Facebook groups (such as local cooking, housewife, and shopping communities) and TikTok product-review hashtags. Consumers will give brutally honest, unfiltered feedback about your product’s packaging, taste, or functional defects long before it reflects in your monthly sales spreadsheets.

⚠️ A Failure Case: The Trap of “Primary-Only” Tracking

- The Blind Spot: Brand leadership assumed the launch was a runaway success based on primary sales. However, by week three, real-time data integration revealed a major discrepancy: while the distributor pipeline was heavily loaded, the secondary offtake (consumer purchases) was incredibly low.

- The Execution Failure: In one key state, the outlet reorder rate was a dismal 11%—meaning 9 out of 10 retailers who received the initial shipment were refusing to buy more. A physical field audit quickly revealed the culprit: only 35% of those outlets had executed the brand’s visibility and shelf-placement guidelines. The product was buried in the back of the shops, and consumers literally did not know it existed.

- The Rescue Pivot: Because they caught this in week three (rather than waiting for a standard 90-day post-launch financial review), marketing paused the volume-linked distributor discounts—which were just building dead stock—and immediately redirected resources toward on-shelf visibility, local retail displays, and in-store sampling. Within five weeks, the outlet reorder rate rebounded to 38%, rescuing the launch from a quiet, expensive failure.

The Egyptian Parallel: If you launch a new beverage or snack across Egypt and measure success purely by how many containers your sales team managed to push into regional wholesale markets in Cairo, Giza, and the Delta, you are set up for a major shock. If the product fails to rotate off the shelves of local corner kiosks or supermarket aisles, those retailers will quickly replace you with a competitor. You must track real-time shelf velocity and be ready to pivot your marketing spend to where the physical friction is occurring.

De-risking Innovation in Egypt Using New Product Development Research

In a fast-moving, unpredictable market, research isn’t an expense—it is an insurance policy. Winners don’t guess what Egyptian consumers want; they build validation engines to prove it.

Don’t leave your next launch up to chance. Partner with experts who understand the street-level realities of local retail.

Ready to de-risk your next launch? Book an exploratory workshop or a tailored consultation today via our NPD Research Service to ensure your product earns a permanent spot in the Egyptian grocery basket.